(Bloomberg) — Asian stocks and European equity futures kept to small ranges as focus turned to upcoming US inflation reports. Japanese government bond yields climbed.

Most Read from Bloomberg

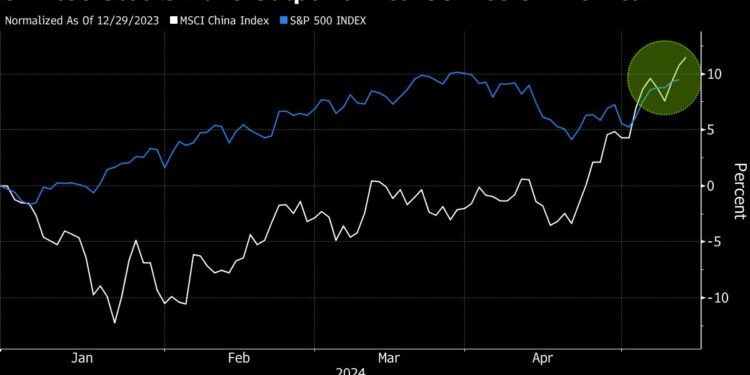

Futures for the Euro Stoxx 50 index stood little changed while contracts for the S&P 500 edged lower. A regional Asian share gauge climbed with Chinese tech shares among the notable gainers. Earnings from tech bellwethers Tencent Holdings Ltd. and Alibaba Group Holding Ltd. are due later Tuesday.

Japan’s 20-year government bond yield rose to its highest level since 2013 on speculation the Bank of Japan will reduce debt-buying amounts at its regular operations again to ease pressure on the ailing yen. The yen extended losses for a third day against the greenback to a two-week low.

A Bloomberg dollar index was flat and 10-year Treasury yields little changed ahead of US producer prices released Tuesday, a key inflation gauge indicator. Federal Reserve Chair Jerome Powell is also scheduled to speak. Consumer price index due Wednesday is projected to show moderation while still remaining too high to warrant rate cuts.

“We’re eyeing US CPI inflation this week to gauge if it will keep coming in hot,” BlackRock analysts including Jean Boivin wrote in a note. “Ultimately, yen weakness is mainly due to the gap between Bank of Japan and Fed policy rates. The yen could recover once the Fed cuts.”

Some prominent trading desks are warning that investors should gear up for a potential break in the calm that’s come over stocks. The options market is betting the S&P 500 will move 1% in either direction after Wednesday’s CPI, according to Andrew Tyler at JPMorgan Chase & Co. On Monday, a Fed Bank of New York survey highlighted an increase in expectations for inflation.

“The key risk is a hotter CPI print,” Tyler said. “But upcoming macro data creates a two-tailed risk — with one tied to stronger-than-expected growth fueling inflation concerns and the other being weaker growth fueling either recession or ‘stagflation’ concerns.”

Back in Asia, any earnings miss from Chinese tech giants may cool the market’s nascent rally. Hong Kong markets are closed Wednesday for a holiday, so reactions to the results will be first seen in the Nasdaq Golden Dragon China Index.

Elsewhere, Australia’s Treasurer Jim Chalmers on Tuesday will announce the government’s books are in the black for a second straight year, putting the nation’s fiscal standing near the top of developed-world counterparts.

On corporate news, market watchers will also be looking for the next step in BHP Group’s takeover battle, after its second approach for rival Anglo American Plc that valued the miner at $43 billion was rejected. Uber Technologies Inc. is buying Delivery Hero SE’s Foodpanda business in Taiwan for $950 million.

In commodities, oil held a gain before the release of OPEC’s market outlook. Iron ore slumped after a major Chinese developer defaulted, the latest sign the debt crisis facing the nation’s steel-intensive property sector is far from over.

Key events this week:

-

Germany CPI, ZEW survey expectations, Tuesday

-

Bank of England Economist Huw Pill speaks, Tuesday

-

US PPI, Tuesday

-

Fed Chair Jerome Powell and ECB Governing Council member Klaas Knot speak, Tuesday

-

China rate decision, Wednesday

-

Eurozone industrial production, GDP, Wednesday

-

US CPI, retail sales, business inventories, empire manufacturing, Wednesday

-

Minneapolis Fed President Neel Kashkari speaks, Wednesday

-

Japan GDP, industrial production, Thursday

-

US housing starts, initial jobless claims, industrial production, Thursday

-

Philadelphia Fed President Patrick Harker speaks, Thursday

-

Cleveland Fed President Loretta Mester speaks, Thursday

-

Atlanta Fed President Raphael Bostic speaks, Thursday

-

China property prices, retail sales, industrial production, Friday

-

Eurozone CPI, Friday

-

US Conf. Board leading index, Friday

Some of the main moves in markets:

Stocks

-

S&P 500 futures were little changed as of 2:42 p.m. Tokyo time

-

Nasdaq 100 futueres were down 0.1%

-

Japan’s Topix was little changed

-

Australia’s S&P/ASX 200 fell 0.3%

-

Hong Kong’s Hang Seng fell 0.1%

-

The Shanghai Composite fell 0.2%

-

Euro Stoxx 50 futures were unchanged

Currencies

-

The Bloomberg Dollar Spot Index was little changed

-

The euro was little changed at $1.0787

-

The Japanese yen fell 0.1% to 156.43 per dollar

-

The offshore yuan was little changed at 7.2429 per dollar

Cryptocurrencies

-

Bitcoin fell 0.7% to $62,654.77

-

Ether fell 0.4% to $2,943.65

Bonds

-

The yield on 10-year Treasuries was little changed at 4.48%

-

Japan’s 10-year yield advanced two basis points to 0.960%

-

Australia’s 10-year yield was little changed at 4.33%

Commodities

-

West Texas Intermediate crude rose 0.2% to $79.24 a barrel

-

Spot gold rose 0.4% to $2,345.63 an ounce

This story was produced with the assistance of Bloomberg Automation.

Most Read from Bloomberg Businessweek

©2024 Bloomberg L.P.